Enabling Google Pay device tokenization

To enable Google Pay device tokenization support for your cards, you need to integrate with one or more supported Token Service Providers (TSP). It is important to note that the issuer has an integration with a TSP and the TSP has an integration with Google. While the end-to-end flow is critical for the user experience, most of the work to enable Google Pay support should be managed directly between the issuer and TSP.

Each TSP shares details about what API methods and fields you must support to enable device tokenization. Within the TSP requirements, you will need to follow some Google Pay specific implementation details for your integration to work properly end-to-end.

Supported Token Service Providers (TSPs)

Google Wallet is available in dozens of countries globally, supported by multiple different TSPs:

- American Express

- Discover

- EFTPOS (Australia)

- Elo (Brazil)

- iD (Japan)

- Interac (Canada)

- JCB (Japan)

- Mastercard

- Paypal (United States and Germany)

- QUICPay (Japan)

- Visa

Brand guidelines

Google's Partner Marketing Hub explains our general branding guidelines and trademark usage guidelines to guide your co-marketing campaigns. The Partner Marketing Hub also includes consumer messaging you can use to describe Google Pay in your creative and promotional materials. If you’d like to use Google Pay branding in any co-marketing materials, you'll need to follow the brand approval process through the Partner Marketing Hub before your campaign goes live. The approval process can require 3-5 days.

Key concepts

Before you get started it is important to understand some key concepts about how Google Pay stores cardholder information and how the Android OS, a user's Google Account, and the payments ecosystem work as components of Google Pay.

Device tokenization

When a user successfully adds their card to Google Pay, Google Pay stores a uniquely generated token on the device that has its own value. This new number, called a dynamic primary account number (DPAN) or device token, is similar to a credit card number.

A DPAN improves account security because Google Pay passes it to a terminal during payment instead of the actual card number. In Google Pay, DPAN is referred as a 'virtual account number'. Users can only see the last four digits of this number, which are visible on the card details view in the Google Wallet app.

Relationship between devices, Android users, Google Accounts and wallets

Users can add a single card to more than one wallet. For example, a user with multiple devices or multiple Google Accounts on the same device can add the same card to each of their respective accounts and devices. Though each user tokenizes a card using the same PAN, each wallet receives a unique DPAN.

Android user

Android devices support multiple users though, in practice, most devices have only one Android user account. User data is stored separately on the device and only one user can be active at a time. When a user unlocks their device, they select an account. The account selected becomes the active user.

Google Account

An Android user can have multiple Google Accounts. For example, a user may have two Google Accounts: a personal Gmail account (personal_email@gmail.com) and a Google Workspace account through their company (company_email@example.com).

Wallet ID

In the context of Google Pay, the wallet ID refers to the container of payments data and tokens on a device. Each Android user and Google Account combination has a unique wallet ID with a 24-byte identifier that is sent during provisioning.

A single Android device can have multiple wallet IDs. For example, a user may have a personal wallet associated with personal_email@gmail.com and a work wallet associated with company_email@example.com. Only one wallet can be active at a time and payment taps use the active wallet.

Google Pay components

On Android devices, Google Pay is divided into two distinct layers that operate together:

- Google Pay service: Part of Google Play Services which is included on most Android devices.

- Google Wallet app: Presents a UI on top of the service.

The Google Wallet app and Google Play services are updated on different cycles and are designed to work flexibly with each other across versions. Google Play services is generally updated every 3-4 weeks and the Google Wallet app is usually updated every 2 weeks. We rely on the solution approvals obtained from TSPs and test that our releases comply with those approvals. We don't notify issuers when updates are mode to Google Play services or the Google Wallet app. These updates generally add new features or are cosmetic changes. If a change breaks an existing integration, Google works with TSPs to make the change and they work with issuers to ensure ongoing support.

Google Pay includes other surfaces:

- Google Pay Website: lets users manage their cards on file and addresses.

- Google Pay iOS app: lets users manage their cards on file and make peer-to-peer transactions.

Google Play services

The Google Pay component of Google Play services manages tokenization, identification and verification (ID&V), token lifecycle management, and payment taps. These features work, even if the Google Wallet app is not installed on the device assuming the user is in a supported country and is using a compatible device.

Google Wallet app

The Google Wallet app provides a more robust UI, loyalty cards, and rich receipts.

Uninstalling the Google Wallet app

The ability to delete or uninstall the Google Wallet app depends on your cardholder's mobile carrier. The original equipment manufacturer (OEM) controls the list of "standard" or pre-installed applications on their device.

- If the Google Wallet app was pre-installed on the mobile device by the OEM, users generally can't delete the app.

- If the Google Wallet app wasn't pre-installed, the user is free to delete it.

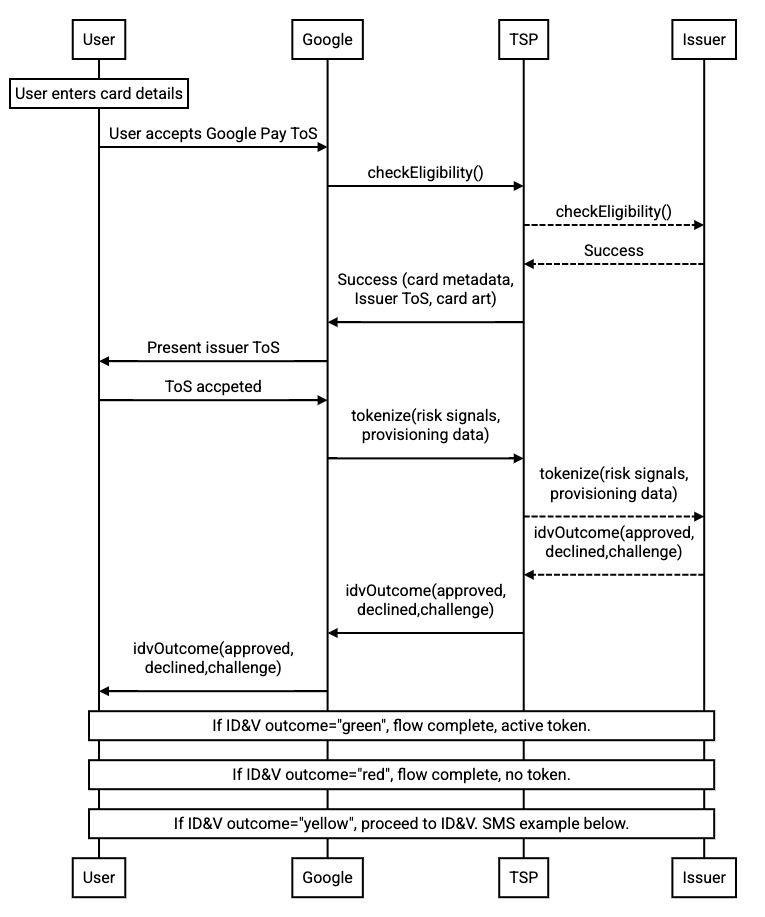

Token provisioning sequence diagrams

The following flow diagrams show how the cardholder's device, Google's servers, the TSP, and the card issuing bank's systems interact to provision a token.

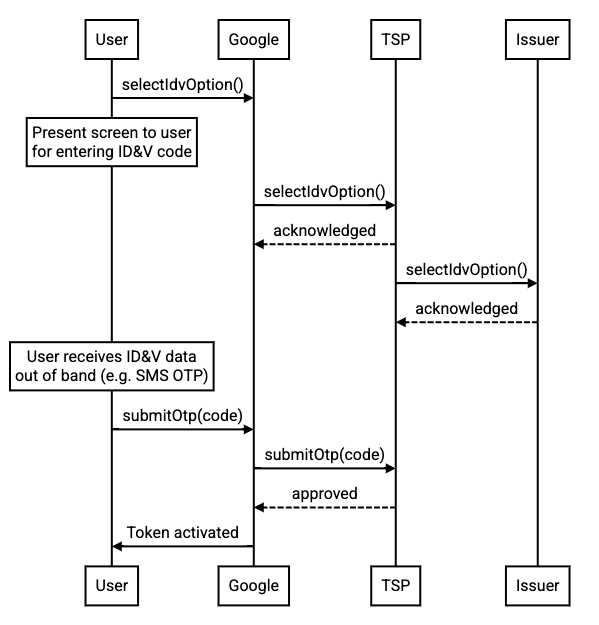

The following flow diagram provides an example for how the yellow path SMS flow works. The flow for each yellow path ID&V option will vary but will generally be similar to the flow below.

Launch checklist

To ensure a smooth launch of your Google Pay integration please ensure you have:

- Signed an NDA with Google

- Signed the issuer agreement with Google

- Completed all functional tests to ensure your tokenization experience is working properly.

- Implemented all applicable Google Pay best practices.

- Implemented at least two yellow path (verification required) authentication options for tokenization.

- Confirmed that no known problems exist related to tokenization, in-store transactions, or online transactions.

- Trained your support team to properly handle and route cardholder inquiries

- Updated your website to inform cardholders about Google Pay as appropriate, including any relevant user-facing Google Pay support information.

- Submitted the list of products to launch in English and in your local language to your TSP. This information will be used to update our supported issuers list.

- Submitted launch checklist documentation with your TSP.

- Received certification from your TSP for launching in production.